Introduction

Carbon emissions are no longer just an environmental issue – they are now a business, compliance and export requirement.

With global regulations like the Carbon Border Adjustment Mechanism (CBAM) and sustainability disclosures such as Business Responsibility and Sustainability Report (BRSR) in India, manufacturing companies must measure and report their greenhouse gas (GHG) emissions.

This process is called Carbon Accounting.

In this guide, we explain:

- What carbon accounting means

- Why Indian manufacturing companies must adopt it in 2026

- Scope 1, Scope 2 & Scope 3 emissions

- Step-by-step carbon footprint calculation

- Reporting & compliance requirements

What is Carbon Accounting?

Carbon Accounting is the process of measuring, tracking and reporting greenhouse gas (GHG) emissions generated by business activities.

It follows global standards like:

- Greenhouse Gas Protocol

- International Organization for Standardization (ISO 14064)

- Global Reporting Initiative (GRI)

- Securities and Exchange Board of India

- European Union

In simple terms:

If your factory consumes fuel, electricity, raw materials or transports goods – you are generating carbon emissions. Carbon accounting measures it scientifically.

Why Carbon Accounting is Important for Indian Manufacturing Companies in 2026

Export Compliance (CBAM Impact)

If you export products like:

- Steel

- Cement

- Aluminium

- Fertilizers

- Electricity

To the European Union, CBAM requires carbon emission reporting.

Without proper carbon accounting:

- Exporter may face additional carbon taxes

- Buyers may reject suppliers

SEBI BRSR Reporting (India)

Under SEBI regulations, the top listed companies must disclose ESG data through BRSR, including:

- Total GHG emissions

- Energy consumption

- Intensity metrics

Carbon accounting becomes mandatory for compliance.

Investor & Buyer Requirement

Large corporations now demand carbon data from suppliers.

If you are a vendor to:

- Automotive companies

- Pharma exporters

- FMCG manufacturers

You will likely be asked for your carbon footprint.

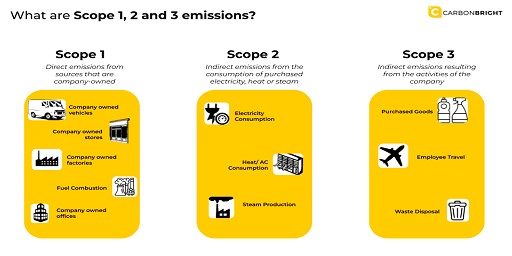

Understanding Scope 1, Scope 2 and Scope 3 Emissions

Scope 1 – Direct Emissions

Emissions from company-owned sources:

- Diesel generators

- Boilers

- Furnaces

- Company vehicles

Example: Diesel used in DG set = Direct emission.

Scope 2 – Indirect Electricity Emissions

Emissions from purchased electricity.

Example:

If your factory consumes 50,000 kWh per month, emissions are calculated using India’s grid emission factor.

Scope 3 – Value Chain Emissions

Indirect emissions from:

- Raw materials

- Transportation

- Waste disposal

- Business travel

- Employee commuting

Scope 3 is the largest and most complex category.

Step-by-Step to Calculate Carbon Footprint

Step 1 – Define Organizational Boundary

Decide:

- Single plant or multiple units?

- Operational control or financial control?

Step 2: Collect Activity Data

Collect:

- Electricity bills (kWh)

- Diesel & fuel purchase records

- Production data

- Transport bills

- Raw material consumption

Step 3 – Apply Emission Factors

Formula:

Emissions = Activity Data ⨯ Emission Factor

Example:

- Diesel used: 1,000 litres

- Emission factor: 2.68 kg CO2/litre

Total Emissions = 1,000 ⨯ 2.68 = 2,680 kg CO2

Emission factors are obtained from:

- IPCC guidelines

- GHG Protocol databases

- Indian grid emission factors

Step 4 – Convert to CO2 Equivalent (CO2e)

Different gases:

- CO2

- Methane (CH4)

- Nitrous Oxide (N2O)

All converted into CO2 equivalent using Global Warming Potential (GWP)

Step 5 – Prepare Carbon Footprint Report

Final report includes:

- Total emissions (tCO2e)

- Scope-wise breakup

- Emission intensity (per ton of product)

- Reduction strategy

Example: Manufacturing Unit Carbon Calculation (Simplified)

| Source | Annual Consumption | Emissions (tCO2e) |

|---|---|---|

| Electricity | 600,000 kWh | 492 |

| Diesel | 12,000 litres | 32 |

| LPG | 5,000 kg | 15 |

| Total | ---- | 539 tCO2e |

This data forms the basis of your carbon report.

Common Challenges Faced by Indian Manufacturers

- Lack of proper data collection system

- No internal ESG team

- Confusion in Scope 3 calculation

- Uncertainty about emission factors

- No knowledge reporting format

That’s where professional carbon consultant support with:

- Data collection templates

- Emission factor databases

- Reporting framework alignment

- Compliance documentation

How Carbon Accounting Connects to ESG & Net Zero

Carbon accounting is the first step toward:

- ESG reporting (GRI / BRSR)

- Net Zero roadmap

- Science-Based Targets

- Carbon credit strategy

Without measurement, reduction is impossible.

Future Outlook (2026 – 2030)

Carbon accounting will become:

- Mandatory for large manufacturers

- Required for export businesses

- Essential for funding & investment

- Standard practice in supply chains

Companies that start early gain competitive advantage.

Conclusion

Carbon accounting is no longer optional for Indian manufacturing companies.

It is:

- A compliance necessity

- An export requirement

- A financial risk management tool

- Sustainability strategy

Starting in 2026, businesses that proactively measure and manage emissions will stay ahead of regulations and market expectations.

Call to Action

If your manufacturing unit needs:

- Carbon Footprint Assessment

- Scope 1, 2 & 3 Calculation

- CBAM Reporting Support

- Carbon Reduction Strategy

Vishwa Environmental Services (VES) can support you with complete end-to-end carbon accounting solutions.

Book a free 20-Minutes Carbon Readiness Assessment for your manufacturing unit.